Introduction: Secured Loans Sound Simple—Until You Look Closer

Secured loans are often explained in just one sentence:

“A secured loan is a loan backed by collateral.”

That explanation is technically correct—and practically incomplete.

Behind that simple definition is a financial tool that can either accelerate stability or magnify mistakes, depending on how it is used. Many people take secured loans without fully understanding the long-term implications. Others avoid them entirely, missing opportunities to reduce costs and build stronger credit.

This article is called “A Brief About Secured Loans” not because the topic is small, but because the concept is often oversimplified.

Here, we take a calm, executive-level look at secured loans—what they are, how they work, when they make sense, and when they don’t. No hype. No fear tactics. Just clarity.

Because the most dangerous financial decisions are usually the ones that feel “obvious.”

What Is a Secured Loan?

At its core, a secured loan is a loan that is backed by an asset.

That asset—called collateral—reduces the lender’s risk. If the borrower fails to repay the loan, the lender has the legal right to seize the collateral to recover losses.

Common examples of collateral include:

- Vehicles

- Property

- Savings or certificates of deposit

- Investments

- Equipment

The presence of collateral changes everything—from interest rates to approval standards to consequences of default.

Why Secured Loans Exist

From a lender’s perspective, secured loans exist for one primary reason: risk management.

Collateral provides:

- A safety net

- Predictable recovery options

- Lower uncertainty

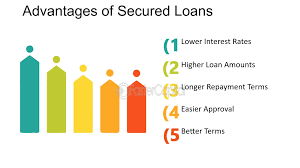

Lower risk for the lender usually means:

- Lower interest rates

- Higher approval chances

- Larger loan amounts

From a borrower’s perspective, secured loans exist to:

- Reduce borrowing costs

- Access capital when credit is limited

- Finance large, long-term purchases

Understanding both sides is essential to using secured loans wisely.

Secured vs Unsecured Loans: The Core Difference

The distinction between secured and unsecured loans defines how they should be used.

Unsecured Loans

- No collateral required

- Approval based mainly on creditworthiness

- Higher interest rates

- Lower risk to personal assets

Secured Loans

- Require collateral

- Lower interest rates

- Higher potential loan amounts

- Higher risk if payments are missed

Neither type is inherently better. They serve different strategic purposes.

Common Types of Secured Loans

Secured loans appear in many forms, often so familiar that people forget they are secured at all.

Auto Loans

Vehicles serve as collateral. Missed payments can result in repossession.

Auto loans are common, but they also demonstrate a key lesson:

collateral that depreciates quickly carries unique risk.

Mortgages

Mortgages are the most widely used secured loans.

Property acts as collateral, enabling:

- Long repayment terms

- Lower interest rates

- Large loan amounts

Mortgages show secured loans at their most structured and regulated.

Home Equity Loans and HELOCs

These loans use home equity as collateral.

They offer:

- Lower rates

- Flexible access to funds

They also put housing security at risk if misused.

Secured Personal Loans

Some personal loans are secured by:

- Savings

- Vehicles

- Other assets

These are often used by borrowers rebuilding credit or seeking lower rates.

Business Secured Loans

Businesses often secure loans using:

- Equipment

- Inventory

- Property

- Receivables

In business contexts, secured loans are part of growth strategy—not emergency funding.

How Collateral Changes Loan Terms

Collateral affects nearly every part of a loan agreement.

Interest Rates

Because the lender’s risk is lower, secured loans typically offer:

- Lower interest rates

- More predictable pricing

This makes them attractive for large or long-term borrowing.

Loan Amounts

Collateral allows access to larger sums. The loan amount is often tied to:

- The value of the asset

- The lender’s risk tolerance

However, higher limits do not mean higher affordability.

Repayment Terms

Secured loans often have:

- Longer terms

- More structured payment schedules

Longer terms lower monthly payments—but increase total interest.

The Real Risk of Secured Loans: Asset Loss

The biggest risk of a secured loan is not the interest rate.

It is losing the collateral.

When borrowers focus only on monthly payments, they forget what is truly at stake.

Losing:

- A vehicle can affect employment

- A home can disrupt stability

- Savings can erase safety nets

Secured loans require a higher level of confidence in repayment ability.

A Leadership Perspective: Collateral Is Not Free

Executives understand that collateral represents stored value.

Using collateral means:

- You are converting stability into leverage

- You are accepting higher consequences for failure

This is not bad—but it must be intentional.

Strong decision-makers never ask, “Can I get approved?”

They ask, “What am I risking—and why?”

When Secured Loans Make Sense

Secured loans are often appropriate when they:

- Significantly reduce interest costs

- Finance long-term value (not short-term consumption)

- Replace higher-risk debt

- Support income-generating assets

Examples:

- Buying a home

- Financing essential equipment

- Consolidating high-interest debt at lower rates

In these cases, the risk is balanced by long-term benefit.

When Secured Loans Are a Bad Idea

Secured loans are dangerous when they:

- Fund lifestyle upgrades

- Cover recurring expenses

- Mask unstable cash flow

- Rely on perfect conditions to succeed

Using essential assets as collateral for non-essential spending is one of the most common financial mistakes.

Secured Loans and Credit Building

Secured loans can help build or rebuild credit when managed well.

They contribute to:

- Payment history

- Credit mix

- Long-term account stability

However, missed payments on secured loans hurt more than unsecured ones—both financially and emotionally.

Consistency is everything.

Secured Loans for Credit Recovery

For individuals rebuilding credit, secured loans can:

- Improve approval chances

- Offer lower rates than unsecured options

- Create structured repayment behavior

But they should be used cautiously, with:

- Conservative loan amounts

- Strong payment automation

- Emergency buffers

Rebuilding credit is about trust—not pressure.

The Psychological Trap of “Lower Interest”

Lower interest rates can create false confidence.

Borrowers sometimes:

- Borrow more than needed

- Extend terms unnecessarily

- Ignore total cost

Leaders look beyond rates. They evaluate risk-adjusted outcomes.

Understanding Loan-to-Value (LTV)

LTV compares loan amount to collateral value.

Lower LTV:

- Lower lender risk

- Better terms

- More borrower safety

High LTV increases danger for both sides.

Healthy secured loans leave margin for error.

Secured Loans in Personal vs Business Contexts

In business, secured loans are often strategic tools.

In personal finance, they are often emotional decisions.

This difference matters.

Businesses plan for:

- Cash flow variability

- Asset depreciation

- Risk mitigation

Individuals should borrow with the same mindset.

Alternatives to Secured Loans

Before using collateral, consider:

- Smaller unsecured loans

- Saving longer

- Adjusting timelines

- Reducing scope

Not every goal requires leverage.

Common Mistakes With Secured Loans

- Using essential assets as collateral

- Borrowing the maximum allowed

- Ignoring worst-case scenarios

- Underestimating long-term cost

- Assuming approval equals affordability

Discipline matters more than access.

Monitoring Secured Loans Over Time

Once a secured loan is active:

- Review balances regularly

- Monitor asset value

- Reassess risk annually

Loans are not “set and forget.”

A CEO View: Secured Loans as Structural Decisions

Secured loans change the structure of your finances.

They introduce:

- Leverage

- Obligation

- Consequence

Strong leaders respect that weight.

They borrow:

- Deliberately

- Conservatively

- With clear purpose

Long-Term Impact: When Secured Loans Go Right

When used well, secured loans:

- Lower financing costs

- Improve credit profiles

- Enable growth

- Increase stability

They quietly support progress.

Long-Term Impact: When Secured Loans Go Wrong

When misused, they:

- Destroy safety nets

- Create cascading problems

- Increase stress

- Limit future options

The difference is rarely the loan itself—it is the decision behind it.

Final Thoughts: Simple Tool, Serious Responsibility

Secured loans are simple in definition but serious in consequence.

They are not shortcuts.

They are not free money.

They are agreements backed by real value.

For beginners, the goal is not to fear secured loans—but to respect them.

Borrow when the outcome strengthens your position.

Pause when it puts essential stability at risk.

That discipline turns secured loans from liabilities into strategic tools.

Word Count:

447

Summary:

Secured loans are loans that are obtainable against any security. But finding a pocket soothing secured loans is not so easy. You have to understand about the secured loans more clearly and that will help you to get the best deal.

Keywords:

Secured loans UK,secured loans,secured personal loans,secured debt consolidation loans uk

Article Body:

These days, more and more people are availing secured loans. But before applying for a secured loan, one needs to have a clear idea about these loans, especially about its basic features, pros and cons, application process etc. Through this article, one can understand secured loans and its features clearly.

What are secured loans?

Secured loans are the loans that are the given to a borrower against a collateral. As a collateral, home or other real estate, automobile, saving accounts, or any valuable objects can be used. With a secured loan, one can borrow up to 125% of his/her collateral that could go up to �75,000. And the repayment period is generally ranged from 5-25 years.

Interest rate on secured loans:

Usually, the interest rate on secured loans is lower than unsecured loans, as these loans are available against a collateral. Besides, if the worth of your collateral is higher than your borrowed amount then lenders may charge a relatively low interest. So, choice of collateral is an important matter to get the best deal.

Purposes for using secured loans:

Wide-spectrum usage of Secured loans has made it more famous nowadays. From, business expansion to higher education, from making your dream home to buying a new car, the list is endlessly increasing. Even, secured loans are provided recently for wedding and holiday purposes as well.

Mindful matters:

The fear factor that inherent with secured loans is collateral repossession. These loans are served to people against their property. Hence, if one cannot repay the amount then his/her property will be repossessed by the lender. So always check your financial capacity before opting for any secured loans. And the amount you want to borrow should be the best answer of repayment question.

For a pocket soothing deal :

A little endeavour will ensure you to get a pocket soothing deal. Look around to get the best deal. Don�t stick to one choice only. But, keep your eyes on other sources too. Many traditional lenders like, banks, lending companies, financial institutions offer various secured loans. Visit them personally and ask for their quotes. Then compare those quotes and then apply.

Online quest:

It is the easiest way to obtain a pocket friendly secured loan. This process is less time consuming and not hampering. You don�t need to go outside to find out the best secured loans. Just fill an online application form and get feedback from online loan lenders directly. Even sometimes, the interest rate on online secured loans is lesser than traditional secured loans.

Against a collateral, one can easily avail any sort of secured loans. Its lower interest rate and flexible repayment period made it very popular nowadays.

Tinggalkan Balasan