Introduction: Personal Loans Are Simple—Until They’re Not

Personal loans are everywhere. Banks offer them. Fintech apps promote them. Friends recommend them. Ads promise fast approval and instant cash.

Yet for something so common, personal loans are often misunderstood.

Many people treat them as emergency money. Others avoid them completely out of fear. Both approaches miss the point.

A personal loan is not good or bad by default. It is a financial tool. And like any tool, its value depends on how—and why—it is used.

This guide is written for beginners, but with a leadership mindset. Not to encourage borrowing, but to help you understand personal loans clearly, so you can make calm, informed decisions instead of emotional ones.

Because the most expensive loan is not the one with the highest interest rate—it is the one you didn’t fully understand.

What Is a Personal Loan?

At its core, a personal loan is straightforward.

A lender gives you a fixed amount of money.

You agree to repay it over a set period of time.

Interest is charged for the use of that money.

Unlike credit cards, personal loans usually:

- Have fixed monthly payments

- Have a defined end date

- Are paid back in installments

This structure makes personal loans easier to plan around—especially for beginners.

Why Personal Loans Exist

From a lender’s perspective, personal loans exist to:

- Generate predictable income

- Manage risk through structured repayment

- Serve customers with diverse needs

From a borrower’s perspective, they exist to:

- Cover large, one-time expenses

- Consolidate debt

- Smooth financial transitions

Understanding both sides helps you choose better.

Common Uses of Personal Loans

Personal loans are flexible by design. Common uses include:

- Debt consolidation

- Medical expenses

- Emergency repairs

- Education-related costs

- Major life transitions

The loan itself does not judge the purpose. The outcome depends on whether the loan improves or weakens your financial position.

The Key Components of a Personal Loan

Before taking any loan, you should understand its building blocks.

1. Loan Amount

This is the principal—the money you receive.

Borrowing more than you need increases:

- Interest paid

- Monthly obligations

- Financial pressure

Experienced decision-makers borrow the minimum effective amount, not the maximum offered.

2. Interest Rate

The interest rate determines how much extra you pay over time.

Rates vary based on:

- Credit history

- Income stability

- Loan term

- Market conditions

Lower rates are better—but only if the loan still fits your budget comfortably.

3. Loan Term

The term is how long you have to repay the loan.

Shorter terms:

- Higher monthly payments

- Lower total interest

Longer terms:

- Lower monthly payments

- Higher total interest

Beginners often focus only on monthly payments. Leaders consider total cost.

4. Monthly Payment

This is where loans become real.

A payment that looks affordable today must remain affordable:

- During income changes

- During emergencies

- During life transitions

A safe rule: loan payments should never require perfect conditions to succeed.

Secured vs Unsecured Personal Loans

Understanding this difference is critical.

Unsecured Personal Loans

- No collateral required

- Based on creditworthiness

- Higher interest rates

Most personal loans fall into this category.

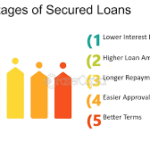

Secured Personal Loans

- Backed by an asset (savings, vehicle, etc.)

- Lower interest rates

- Higher risk if payments are missed

Secured loans reduce lender risk—but increase personal risk.

How Credit Impacts Personal Loans

Your credit profile strongly influences:

- Approval chances

- Interest rates

- Loan limits

Credit is not a judgment of character. It is a record of behavior.

Consistent, predictable behavior lowers risk in the lender’s eyes—and lowers costs for you.

Fixed vs Variable Interest Rates

Most personal loans have fixed rates, which means:

- Payments stay the same

- Planning is easier

- Risk is lower

Variable rates can change over time. For beginners, predictability is usually the safer choice.

The Application Process: What to Expect

Applying for a personal loan typically involves:

- Income verification

- Credit check

- Identity confirmation

Approval speed varies. Faster is not always better.

Good decisions are rarely rushed.

Understanding Fees and Fine Print

Interest is not the only cost.

Watch for:

- Origination fees

- Prepayment penalties

- Late payment fees

A slightly higher interest rate with fewer fees can be cheaper overall.

Always calculate the true cost.

When a Personal Loan Makes Sense

A personal loan can be a smart choice when it:

- Replaces higher-interest debt

- Covers unavoidable expenses

- Creates long-term financial stability

The loan should solve a problem, not postpone it.

When a Personal Loan Is a Bad Idea

A personal loan is risky when it:

- Funds lifestyle inflation

- Covers recurring expenses

- Masks deeper financial issues

Borrowing to maintain appearances is one of the most expensive habits people develop.

Personal Loans and Debt Consolidation

Debt consolidation is one of the most common—and misunderstood—uses.

It works best when:

- Interest rates are significantly lower

- Spending habits change

- Payments become simpler

Without behavior change, consolidation only delays problems.

Budgeting Around a Personal Loan

Before accepting a loan, simulate life with the payment.

Ask:

- What happens if income drops?

- What expenses could increase?

- Is there room for error?

Strong plans assume imperfection.

The Psychological Side of Borrowing

Debt affects emotions.

Some people feel relief.

Others feel pressure.

Understanding your emotional response helps prevent mistakes.

Calm borrowers make better decisions than stressed ones.

Paying Off a Personal Loan Faster (If You Can)

Extra payments reduce interest—but only if:

- Emergency savings are intact

- No higher-interest debt exists

Speed is good. Stability is better.

How Personal Loans Affect Credit Scores

Personal loans can:

- Improve credit mix

- Build payment history

- Increase total debt

On-time payments help. Missed payments hurt—especially early.

Consistency matters more than speed.

Alternatives to Personal Loans

Before borrowing, consider:

- Emergency savings

- Payment plans

- Lower-interest options

Loans are tools—not defaults.

Choosing the Right Lender

Not all lenders are equal.

Look for:

- Transparency

- Reasonable terms

- Strong customer support

Trustworthiness matters when problems arise.

A CEO Perspective: Loans as Strategic Tools

Leaders do not fear loans—but they respect them.

They ask:

- What problem does this solve?

- What risk does it introduce?

- What happens if conditions change?

This mindset protects long-term stability.

Common Beginner Mistakes

- Borrowing the maximum offered

- Ignoring total interest

- Rushing decisions

- Focusing only on approval

Approval is not success. Repayment is.

Building Confidence With Personal Loans

Used well, a personal loan can:

- Improve credit

- Reduce stress

- Increase financial control

Used poorly, it creates long-term friction.

The difference lies in intention and discipline.

The Long View: Loans Come and Go, Habits Stay

A personal loan ends.

Financial habits continue.

Strong habits turn loans into stepping stones instead of stumbling blocks.

Final Thoughts: Borrow With Clarity, Not Emotion

Personal loans are neither traps nor solutions by default.

They are agreements—clear, structured, and predictable.

For beginners, the goal is not to avoid loans entirely, but to understand them deeply enough to use them wisely.

Borrow when it strengthens your position.

Pause when it doesn’t.

That simple discipline is what separates financial stress from financial confidence.

Word Count:

597

Summary:

If you�re looking to borrow a sum of money then the chances are that you�ll look to take out a personal loan rather than any other type. The term personal loan is simply used to describe standard types of borrowing � i.e. a loan taken out by a consumer rather than a business for general purposes (but not for a mortgage which is obviously dealt with by a mortgage loan).

The majority of personal loans can be used for any purpose and the chances are that your lender won�t eve…

Keywords:

loans,life,insurance,assurance,personal,journalist,finance,uk

Article Body:

If you�re looking to borrow a sum of money then the chances are that you�ll look to take out a personal loan rather than any other type. The term personal loan is simply used to describe standard types of borrowing � i.e. a loan taken out by a consumer rather than a business for general purposes (but not for a mortgage which is obviously dealt with by a mortgage loan).

The majority of personal loans can be used for any purpose and the chances are that your lender won�t even be hugely interested in what you want the money for. Their primary concern is checking that you�ll be able to repay your loan! This situation can be different with specialist loans (which also fall under the banner of personal loans) such as home improvement loans and car loans, for example. These loans are expected to be used for their specified purpose � i.e. a major DIY project or a car purchase.

Apart from this fact the majority of personal loans work in much the same way. You apply for your loan, get your money and then spend it as you intended. You will then make a regular payment (usually on a monthly basis) to your lender to repay the money you borrowed for the period of time in your loans agreement. This payment will be made up of a sum of money that goes to pay off the original sum you borrowed plus a sum that goes towards paying off the interest you�ll be charged. So, at the end of your loan term you�ll have repaid your original borrowings and the interest attached to your particular loan.

One difference worth noting here is that between unsecured and secured personal loans. Unsecured loans are given to consumers without security (or to those that choose not to use available security to get a loan). These loans will generally have higher interest rates attached to them than secured loan options and you may be restricted in how much you can actually borrow here. Secured loans, on the other hand, will have lower interest rates and can be taken out for higher sums. The reason behind this is the fact that this kind of loan will use your property (usually your home) as a guarantee against your loan. So, if you default on your repayments your lender has a cast-iron guarantee that they will get their money back via the property you used as security.

If you aren�t a home owner then you will generally be restricted to taking out unsecured loans here but, if you do own your own property, then you�ll have to make a choice between a secured or unsecured loan. This really boils down to personal preference and how comfortable you are using your home as security in order to get a better deal. In the majority of cases this isn�t an issue and most people will opt for secured loans to get the right kinds of rates and loan amounts for their purposes.

Do be careful to make sure that you understand both how personal loans work and how to get the best rates for the loans you take out before you sign up to anything. There are hundreds of sites on the Internet that can give you more detailed information or that can even help you apply for a loan � take a look online for personal loans in a UK search engine (such as msn.co.uk for example) before you start for some useful information.

Tinggalkan Balasan